Methodology

This report was prepared by the Drofa Comms research team between early and mid-2026. It draws on three principal sources. They include publicly available market data and regulatory developments spanning 2024 to early 2026; published statements, product announcements, and investor communications from major centralised exchanges, such as Coinbase, Bitget, Binance, Kraken, and OKX; and primary research comprising structured written questionnaires completed by senior representatives of participating exchanges. The questionnaire addressed strategic priorities, product direction, user expectations, AI deployment, and regulatory positioning.

The report focuses on centralised exchanges active in spot and derivatives markets. It does not examine decentralised exchanges, DeFi protocols, or crypto custody providers. All external sources are cited in the text. The findings are intended to give practitioners and observers a grounded reference for understanding where crypto exchanges in 2026 stand and where the competitive pressure is coming from.

Introduction

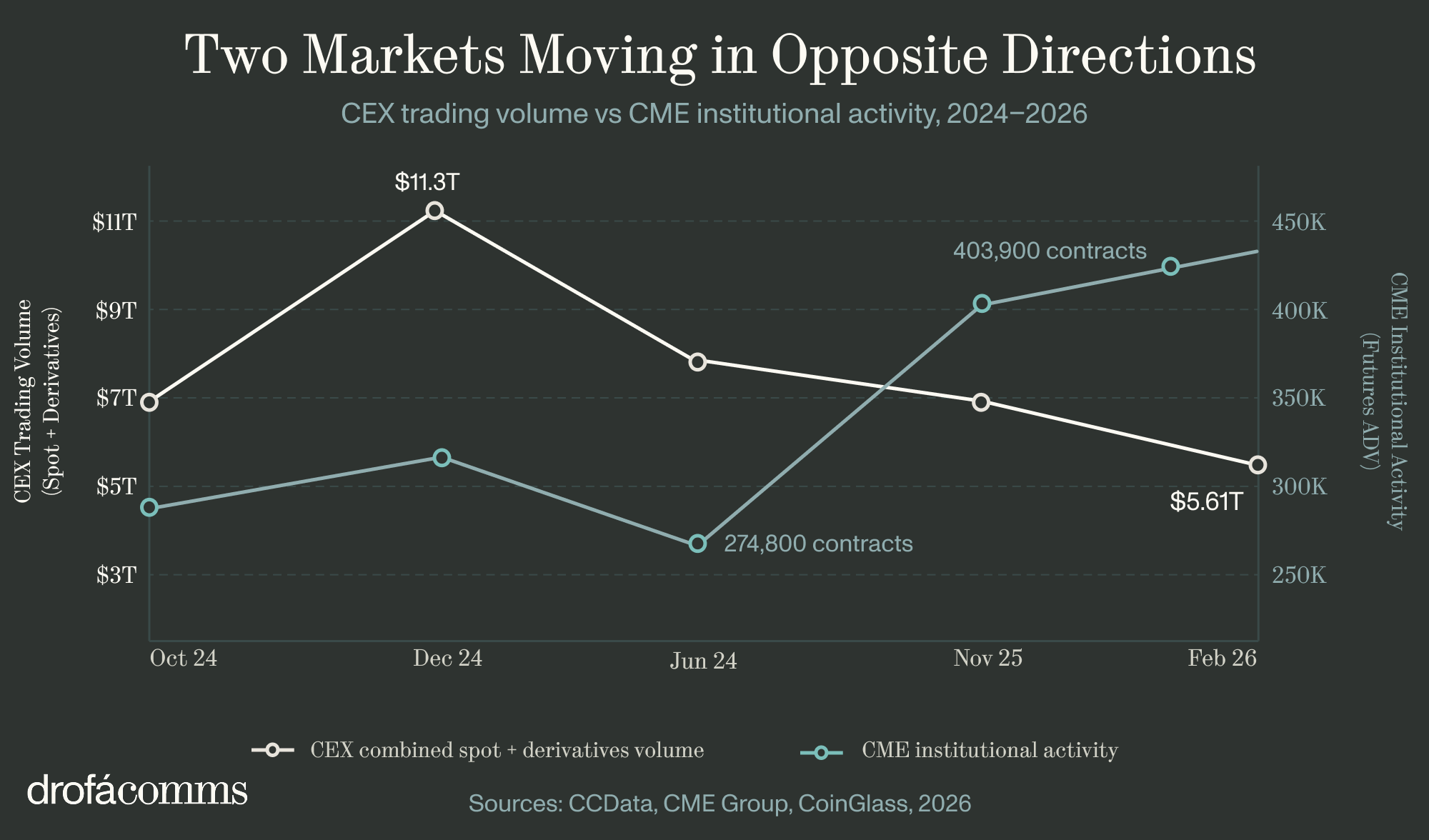

In 2026, centralised crypto exchanges are entering a different phase of market development. Trading volumes have remained uneven, with combined spot and derivatives volume falling to $5.61 trillion in February 2026, the lowest level since October 2024 and roughly half the all-time high of $11.3 trillion recorded in December 2024. At the same time, institutional participation continued to expand. CME’s crypto futures average daily volume reached 403,900 contracts in early 2026, up from roughly 274,800 a year earlier, a 47% year-on-year increase. The market is therefore undergoing a change in composition. Retail volume has receded, while institutional participation has continued to advance, placing exchanges that intermediate this capital under more demanding standards of safety, reporting, and execution.

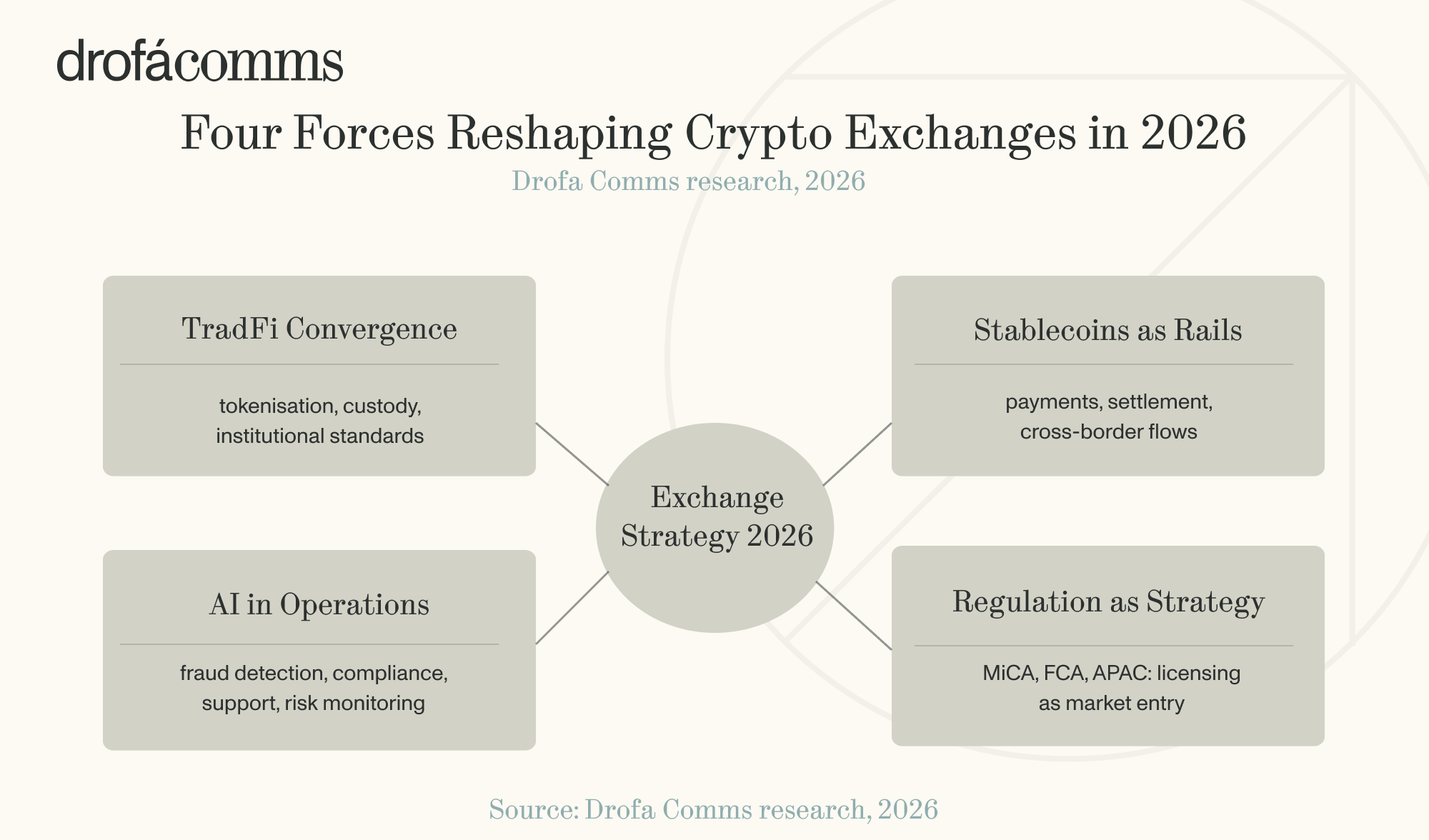

Several forces are driving this transition. The convergence of crypto and traditional finance has brought institutional capital, and with it institutional requirements, directly into the exchange sector. Stablecoins have moved beyond their earlier role as trading instruments and are increasingly embedded in payment and settlement infrastructure, creating new operational demands for exchanges. AI has shifted from promotional language to operational deployment across fraud detection, compliance screening, and customer support. Regulation, meanwhile, is determining which exchanges can access new markets, launch products, and attract institutional clients, making licensing an increasingly important condition of commercial expansion.

In this environment, exchanges face a central question: what will it take to remain competitive through 2030 and move ahead of peers?

This report addresses that question. Based on the evidence examined, it identifies three distinct strategic archetypes within the crypto exchange sector, outlines a forward view to 2030, and sets out recommendations for exchanges seeking to preserve competitiveness over the long term.

The Forces Reshaping Crypto Exchanges in 2026

These four forces are not operating in isolation. Taken together, they are narrowing the space in which exchanges can avoid making explicit strategic choices — about which clients to serve, which products to build, and which regulatory frameworks to operate within. Understanding each force individually is a starting point. The more consequential question is what they require of exchanges in combination.

Crypto and Traditional Finance Are Merging

Crypto, once positioned as a parallel layer to the broader financial system, is now converging with it. Bitget’s trajectory over the past year illustrates what that convergence looks like when an exchange commits to it systematically. The platform moved in stages: first integrating on-chain trading capabilities, then launching tokenised equity linked trading products, then introducing CFD trading in late 2025 to bring equities, commodities, and forex onto the platform using stablecoin-based settlement. A partnership with Ondo followed, giving users access to tokenised assets including US stocks and ETFs. So, by early 2026, Bitget restructured its positioning entirely. It places a TradFi tab alongside crypto trading as an equal product category.

The commercial results of this strategic move have followed. Cumulative trading volume for tokenised stock futures crossed $15 billion. Daily TradFi volume reached $4 billion within weeks of the public launch, later hitting a single-day record above $6 billion. Institutional spot trading volume rose from 39% of the platform’s total in January 2025 to 82% by December — a recomposition of the user base that reflects deliberate product direction rather than market drift. Meanwhile, the broader tokenised equities market reached more than $960 million in assets under management by January 2026, up from $32 million at the start of 2025, nearly 3,000% growth in twelve months. As Gracy Chen, CEO of Bitget, puts it: “The next phase of exchange infrastructure will be defined by platforms that allow assets from both worlds to coexist seamlessly within a single trading environment.”

Bitget is not alone in this direction, but it is among the furthest along in executing it. Kraken in May 2025, completed the $1.5 billion acquisition of NinjaTrader, the leading US retail futures platform, gaining a CFTC-registered licence and access to nearly two million traditional futures traders in a single transaction rather than through staged product development.

This visible confluence is dissolving the boundary between a crypto trading venue and a broader financial platform. This occurs because each side still possesses capabilities the other cannot readily reproduce. Traditional finance retains the institutional foundations of market trust. They have regulatory standing, established custody standards, client relationships, and enormous balance sheets. Crypto contributes technological advantages that the traditional system has struggled to build natively. It includes programmable settlement, continuous 24/7 market access, and global reach with fewer intermediating layers. Neither side, acting alone, fully meets the requirements of the next phase of financial market development. Convergence, as a result, is becoming a strategic inevitability.

Stablecoins Are Becoming the Standard for Payments

Stablecoins are not confined to trading activity anymore. They are now increasingly tied to payments, settlement, treasury operations, and cross-border transfers. In its March 2026 report, FATF stated that, as of mid-2025, more than 250 stablecoins were in circulation, with total market capitalisation exceeding $300 billion. In the UK, the FCA has also made stablecoin payments a 2026 priority and selected four firms to test stablecoin use cases within its regulatory sandbox.

On the commercial side, stablecoins are already being utilised to settle invoices, manage international payroll, and rebalance treasury positions across regions within minutes. Japan’s three largest banks, for example, joined a pilot platform using stablecoins for cross-border payments by linking blockchain infrastructure with SWIFT. Payment firms are moving in the same direction. Stripe has rolled out stablecoin accounts across 101 countries, while Visa’s stablecoin settlement volumes have reached an annualised run rate of $4.5 billion.

This development is putting a direct pressure on exchanges. They are having to invest more heavily in on- and off-ramp infrastructure, expand payment gateway coverage, and build partnerships capable of supporting stablecoin integration at scale. As a result, stablecoin functionality is becoming part of the underlying financial architecture exchanges are expected to support.

AI Is Entering Core Operations

For several years, AI in crypto was often framed more as a narrative than as a measurable operating capability. By 2026, that has changed. AI is now embedded in the way many exchanges detect fraud, process compliance, manage risk, and handle customer support.

The drivers are concrete. Crypto theft totalled around $3.4 billion in 2025, while AML and KYC penalties across the crypto sector exceeded $927 million in the first half of 2025 alone, with regulatory penalties across financial services rose sharply over the same period. For exchanges, the consequence is direct: where suspicious activity cannot be detected and addressed quickly, the cost is paid in fines, financial losses, and reputational damage.

AI is primarily being used to close that gap. It identifies complex patterns associated with money laundering, detects emerging fraud methods before they become widespread, and reduces false positive alert rates. TRM Labs has stated that AI’s most visible impact is in suspicious activity detection, through faster filtering, fewer false alerts, and quicker response times.

Its role extends beyond compliance. By 2026, AI-powered support agents across financial services are automating 80% to 90% of routine customer cases. These cases include onboarding, fee disputes, and withdrawals. Human teams, by contrast, focus on more complex matters. On the trading side, AI is being used to scan liquidity across order books, exchanges, and chains. It is routing transactions in ways that reduce slippage and latency in real time.

These examples show that AI is already present across multiple exchange functions. The more important question is where it is being applied and how strong the evidence is for its impact. The results so far come from adjacent parts of financial markets. Nasdaq reported a 20.3% improvement in order execution quality after moving to a reinforcement learning model, a result that is quantified, peer-reviewed, and directly relevant to exchange operations. Coinbase has also stated that its AI-based fraud detection outperformed legacy rule-based systems in lowering both losses and operating costs, although the underlying performance data has not been published.

Exchanges report deploying AI in surveillance, compliance screening, and support triage. The direct responses gathered for this report confirm that. Even so, published and quantified benchmarks from crypto-native deployments remain limited. Crucially, the functions where exchanges deploy AI, namely high-speed pattern recognition, large-scale alert filtering, and real-time decision support, are the same functions where traditional finance has already shown measurable gains. On that basis, the expectation that crypto exchanges will achieve comparable outcomes is well founded. That is even despite sector-specific evidence remains less developed.

Regulation Is Defining Market Entry and Growth

In many jurisdictions, oversight of the crypto sector was previously shaped more by court decisions, enforcement actions, and regulatory ambiguity. By 2026, that condition is changing. The policy shift in the United States during 2025 has become one of the markers of that transition.

In July 2025, the US President signed the GENIUS Act, the first major federal crypto legislation in US history. It established a regulatory framework for dollar-backed payment stablecoins. It requires one-to-one reserve backing and monthly disclosures, and brought long-awaited clarity to a $250 billion market. Shortly thereafter, the House passed the CLARITY Act with bipartisan support. It aims to resolve the longstanding dispute between the SEC and CFTC over regulatory jurisdiction for digital assets. When the United States moves at the federal level, it often affects how other jurisdictions behave.

In the EU, MiCA has introduced a single licensing and oversight framework, with ESMA maintaining a public register of authorised providers. As for the UK, the FCA is building a full domestic regime, with a formal application period beginning in late 2026 and the broader framework expected in October 2027. In Hong Kong, the SFC is permitting licensed platforms to offer perpetual contract models subject to defined investor protection rules.

Taken together, these developments are changing what regulation means for exchanges. A licence was once treated primarily as a compliance requirement. It is now a route to market access, product eligibility, partnership credibility, and institutional trust. Delays in obtaining appropriate regulatory status create commercial obstacles. It also pushes activity offshore and sustains uncertainty that institutional investors are reluctant to accept. The broader trajectory points toward a more credible market structure. This is the one in which higher entry standards gradually remove weaker participants and strengthen the conditions for institutional confidence.

How Crypto Exchanges in 2026 Are Rebuilding for a Harder Market

Where Crypto Exchanges Are Placing Their Bets in 2026

Every exchange is pursuing growth. The difference lies in the strategies chosen to achieve it, because the market is now pulling in two directions at once.

Institutions are allocating capital to crypto at scale. Yet, they expect custody standards, reporting systems, segregated accounts, and settlement clarity that many exchanges were not originally built to provide. At the same time, retail participation is narrowing in size. Meanwhile, it becomes more concentrated in larger balances. This makes remaining users more selective about the platforms they stay with. Serving both groups equally well through a single undifferentiated product is becoming utterly difficult.

What distinguishes the exchanges moving with the greatest confidence is that they have made an identifiable choice about which direction to lean into. Some are expanding their offering to play a broader financial role. Coinbase, for example, is building what it calls the “Everything Exchange,” combining stablecoin infrastructure, payment rails, and wider financial activity on a single platform. Others are leaning more directly into institutional demand. Kraken is pursuing a similar course through the expansion of prime brokerage, custody, and OTC services for high-volume professional clients.

At the same time, some exchanges are not organising purely around the institutional-retail divide. KuCoin’s CEO, BC Wong, states that the platform aims to “build trusted digital asset infrastructure for a global user base,” a formulation that places reliability and reach at the centre of strategy. Bitunix reflects a different approach. Rather than competing directly for the same users as the largest global platforms, it is going deeper in markets that large exchanges often overlook, specifically active professional traders in Southeast Asia and Latin America, where access to advanced trading tools remains limited. As Bitunix describes it, the objective is “sustainable active trader growth, with a focus on underserved prosumers.”

The broader point is that the leading exchanges are no longer trying to compete through broad similarity. They are making more deliberate decisions about whom they intend to serve, which capabilities they need to build, and where lasting competitive advantage is likely to emerge.

Building for Institutional Demand

Institutional participation has become a core strategic priority for crypto exchanges in 2026. Institutions still want exposure to crypto. Even so, the more important issue is whether exchanges can support that exposure under the governance, custody, reporting, and regulatory conditions institutions require.

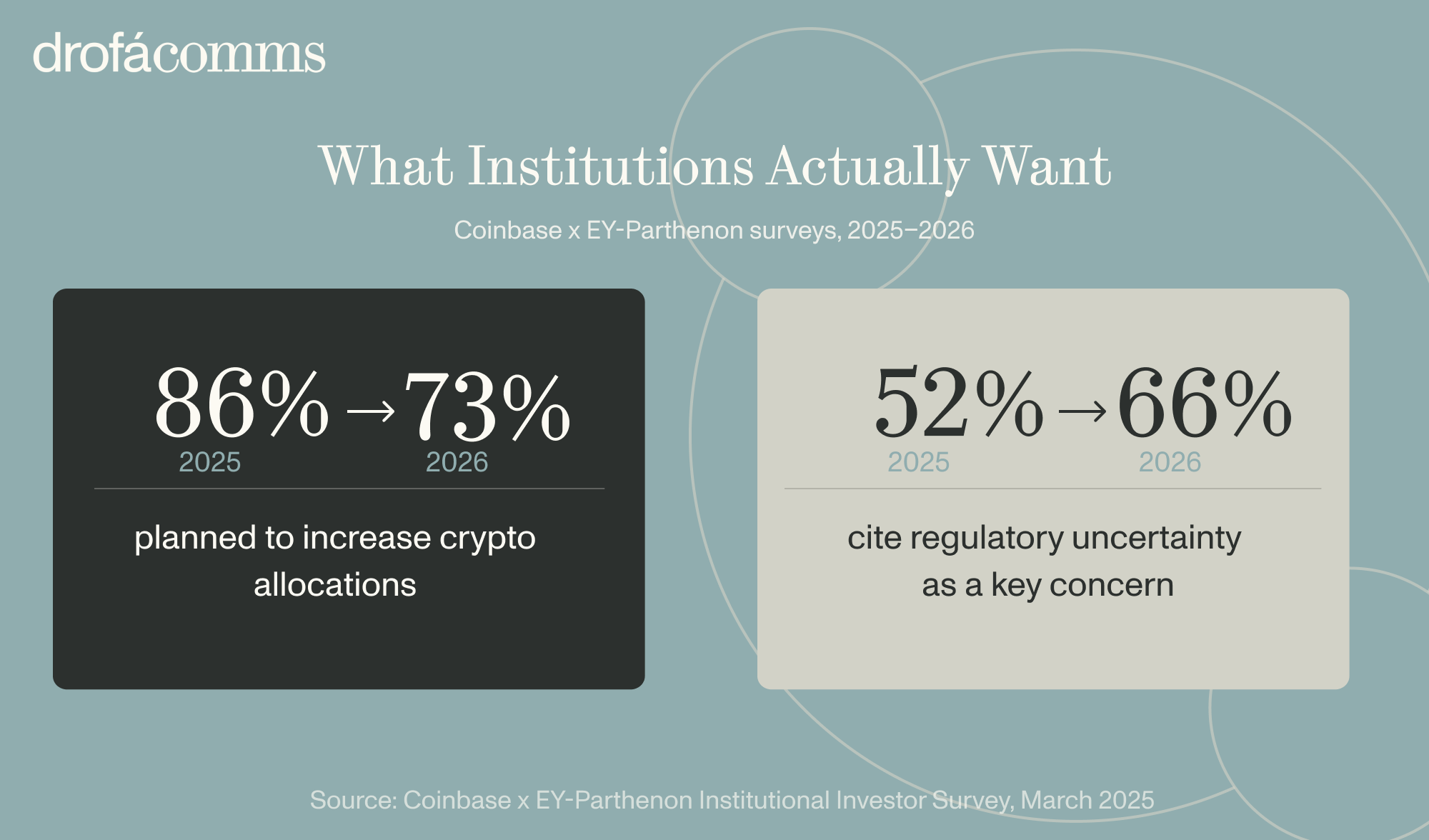

The 2025 and 2026 Coinbase / EY-Parthenon surveys illustrate this shift directly. In 2025, 86% of respondents said they planned to increase their crypto allocations. By 2026, that figure had declined to 73%. At the same time, the share naming regulatory uncertainty as a key concern rose from 52% to 66%.

A superficial reading of these figures would suggest that institutional demand is weakening. Fewer investors plan to increase exposure, while more cite regulation as a barrier. That interpretation is plausible, but incomplete. The 73% figure still represents a clear majority planning to grow crypto allocations, a level that would itself have appeared notable only a few years earlier. What has changed is less the direction of institutional interest than the conditions attached to it. In 2025, the dominant theme was expansion of exposure in itself. By 2026, the emphasis had shifted to the terms under which capital can be deployed: stronger controls, tighter governance, and more resilient counterparties. The movement from 86% to 73% is best understood as a filtration of intent. Institutional capital has not withdrawn from crypto, but has become more selective about how and where it enters.

This shift is already reflected in the exchange strategy. Kraken’s MiCA-aligned custody expansion in Europe emphasises consistent reporting and security standards across jurisdictions. Binance has gone further, building a third-party custody model that holds client assets in separate bank accounts and separates custody from execution. The common objective is to reduce counterparty risk to a level institutional clients can accept. Bitget has pursued institutional readiness through a different sequence. In June 2025 it launched Bitget PRO, a dedicated programme for institutional and high-volume clients offering custody and loan services, OTC infrastructure, and API capacity suited to programmatic trading. It simultaneously partnered with Cobo and Fireblocks to add a custody layer built on institutional-grade security standards. OKX in October 2025 launched Rubix, a digital assets-as-a-service platform designed to let regulated financial institutions offer digital asset services to their own clients, without building the underlying infrastructure themselves.

As a result, exchanges seeking institutional clients are having to integrate stronger custody arrangements, transparent asset segregation, and regulated product access. Those are the areas where institutional standards are now being set.

Reworking the Retail Experience

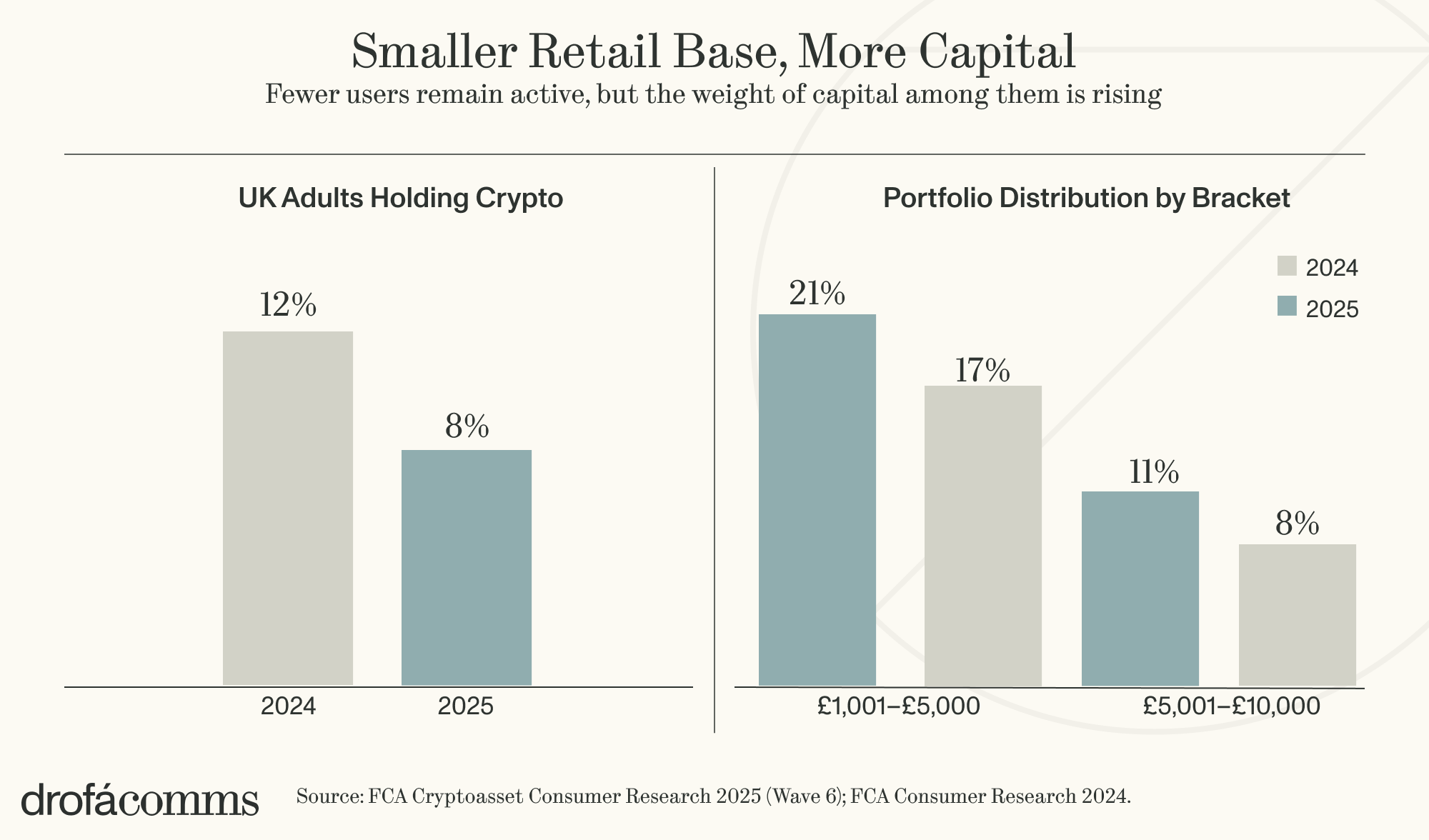

Retail activity remains a significant component of the centralised exchange business. According to the FCA, 73% of UK retail users acquire crypto assets through centralised exchanges, up four percentage points from 2024. Yet the composition of that retail base is changing, and the consequences for exchanges are direct.

The share of UK adults holding crypto assets fell from 12% in 2024 to 8% in 2025. At the same time, holdings in the £1,001 to £5,000 range rose by four percentage points to 21% of users, while the £5,001 to £10,000 bracket increased by three percentage points to 11%. The retail base is therefore shrinking in breadth while becoming more concentrated in users holding larger sums. One plausible explanation is that more casual market participants, particularly those who entered during the 2021 bull cycle, have exited as conditions became less favourable. The FCA’s own findings are consistent with this view, showing that while fewer people remain active in crypto, those who do are committing more capital and behaving more deliberately.

In this context, balance size is not a single thing that defines a serious retail user. Around 63% of crypto users state that they are willing to take higher risks for higher returns, compared with 24% among those who are aware of crypto but do not hold it. They trade more frequently, use more platform features, and are markedly less tolerant when things go wrong. Users who rank ease of use, platform reputation, and security as core reasons for choosing an exchange are not behaving like users drawn in by marketing alone.

Bitunix describes this profile as expecting “more advanced features combined with faster execution and a truly all-in-one trading environment.” KuCoin frames the same issue through the drivers of retention, pointing to “asset protection, execution reliability, platform stability, and transparency.”

Both responses indicate that serving retail users in 2026 depends less on acquisition alone and more on how the platform performs at moments of friction. Downtime during volatility, delayed withdrawals, and weak support responses are the failures serious users remember. They increasingly shape which platforms those users remain with.

Chasing Payment and B2B Ambitions

The payments problem remains acute in many emerging markets. Nearly 1.3 billion adults globally remain unbanked. But the absence of bank accounts does not mean the absence of financial activity. Remittances, payroll, and everyday payments still move through these populations. They typically come via cash, informal networks, or transfer services. They, in turn, charge fees well above what formal banking would. In Southeast Asia, where more than 70% of adults are unbanked or underbanked, that friction is particularly visible. The region is simultaneously among the fastest-growing crypto markets in the world. APAC records a 69% year-on-year increase in on-chain activity in the 12 months ending June 2025. The combination means that where conventional banking infrastructure is slow, costly, or absent, crypto can fill part of the gap, but only if exchanges make that access workable for people who have never had a bank account.

As Bitunix CSO, Steven Gu, puts it, “Cashing in is the hurdle.” Converting local currency into crypto, and back again, often means relying on slow bank transfers, expensive conversion channels, or no direct banking integration at all. Traditional remittance systems still charge roughly 6.5% per transaction on average. For users in these markets, the cost and friction of moving money in and out of a platform frequently determine whether the platform is usable in practice.

Exchanges are responding with more concrete measures. Krak, Kraken’s payments app launched in June 2025, already supports transfers across more than 160 countries and over 300 assets in fiat, crypto, or stablecoins. Binance has addressed this issue through its P2P marketplace that lets users in emerging markets buy and sell crypto directly through local payment rails and it does not require a bank account at any point in the transaction. Bitunix is partnering with local payment applications and banking networks in its target markets to “make local-currency deposits as simple as a mobile top-up.” KuCoin likewise points to rising user demand for “clearer pathways between trading activity and real-world utility, such as payments and financial services.”

This is changing how exchanges define the product itself. Payments infrastructure is becoming a core component of the offering, and as that happens, exchanges are moving closer to financial super-apps than to pure trading venues.

Using Compliance to Enter and Grow

For exchanges, regulatory approval was once treated primarily as an obligation. It still serves that function. But it is now also part of market-entry strategy, product expansion, and commercial positioning.

A licence strengthens an exchange’s standing with banks, payment providers, and distribution partners. Other than that, it provides institutional clients with evidence that the platform meets the standards required to support deployed capital. The 2026 EY / Coinbase institutional investor survey found that 66% of respondents identified regulatory compliance as a key factor in choosing a custodian, up from 25% a year earlier. Therefore, regulatory status has become one of the more decisive variables in how institutions select service providers.

In 2026, exchanges gain an advantage when they secure the relevant licences before entering a market. Several have already shown what that looks like in practice. In June 2025, Coinbase secured a MiCA licence from Luxembourg’s CSSF, gaining access to all 27 EU member states through a single authorisation. Kraken, in turn, used its MiFID II structure to expand regulated derivatives access across the EEA.

Among the exchanges that provided direct input to this report, compliance is treated as decisive both in partner selection and in user growth strategy. Bitunix filters partnerships by compliance alignment, favouring firms that “prioritise regulatory standards over short-term volume.” KuCoin positions compliance as a core strategic pillar, shaping how it enters and operates across markets. As they put it: “Rather than simply enabling access, compliance serves as the foundation for building trusted infrastructure.”

Across the examples, it is indisputable that compliance is not being evaluated only as a cost restriction anymore. It is morphing into a durable commercial asset, strengthening market access, partner credibility, and product reach.

Embedding AI Into Daily Work

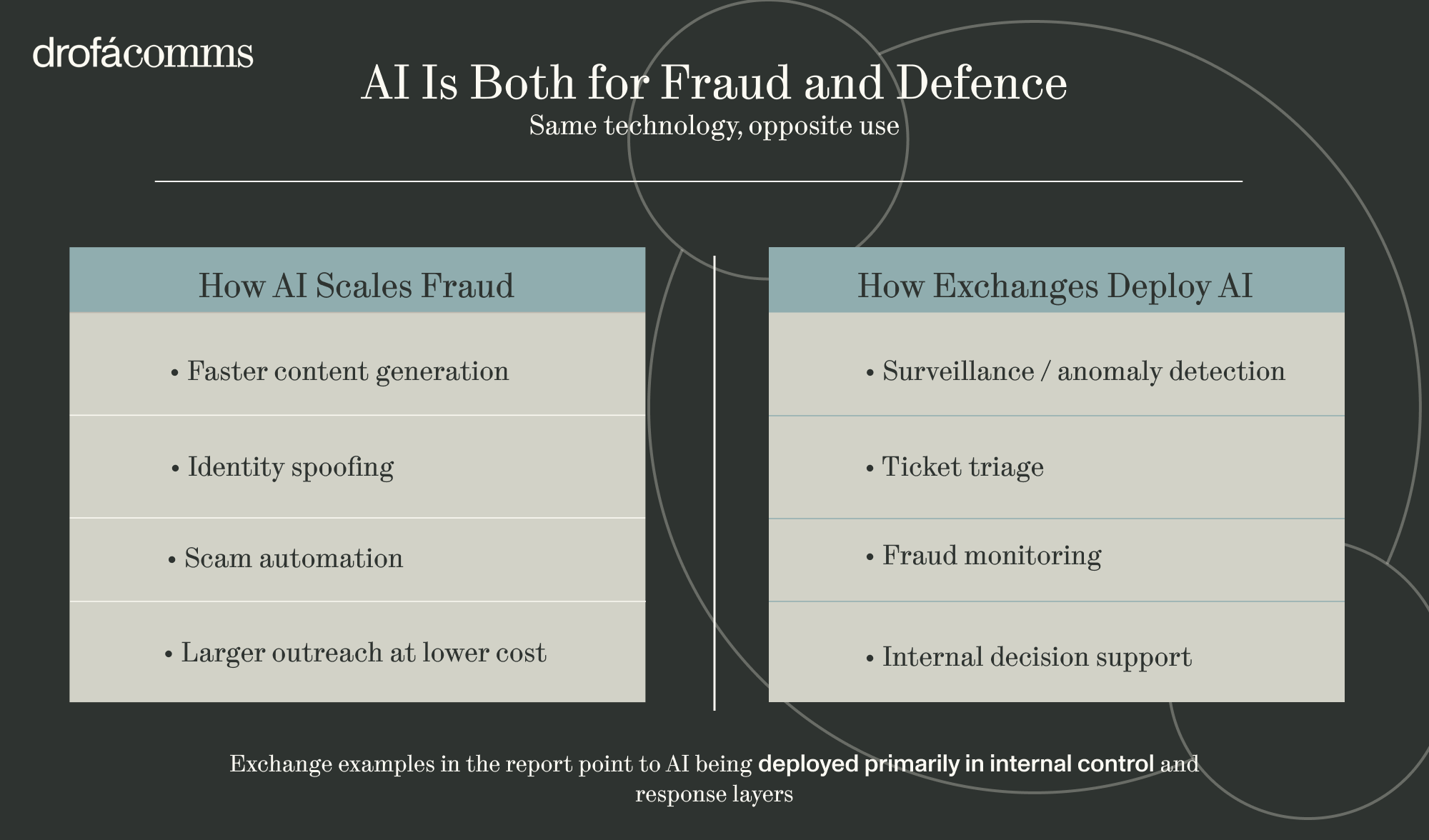

The push to embed AI into exchange workflows is being driven by more than fraud alone, although fraud remains part of the story. In 2024, at least $10.7 billion was sent to crypto fraud schemes globally, according to TRM Labs. AI has contributed to that scale by enabling scam networks to generate phishing emails, fake investment sites, and multilingual messages at a speed and volume that were previously harder to achieve.

Exchanges, however, deploys the same technology in response. Within internal systems, they use AI to identify suspicious behaviour earlier, strengthen transaction monitoring, support compliance screening, and sort routine service requests before they reach human teams. Its value is greatest in precisely those functions. Speed, volume, and pattern recognition, where manual processes perform least effectively, define them.

Bitunix describes AI as its “Efficiency Engine.” Steven Gu characterises the change in fraud and compliance work as a shift “from being reactive to predictive,” with the emphasis on identifying suspicious behaviour before losses occur. KuCoin describes a similar use case, stating that: “AI systems can identify abnormal transaction patterns in real time, flag potential fraud risks, and support early intervention before losses occur. They also help support teams prioritise and resolve user issues more efficiently, allowing human staff to focus on complex cases that require judgment.”

In both accounts, AI is in the underlying operating model, especially in surveillance, ticket triage, and internal decision support. Across the exchanges examined in this report, the strategic differences do not lie primarily in whether an exchange uses AI. They are in what each exchange has chosen to compete on. Some are building the infrastructure that makes them relevant to institutions and regulated markets. It includes custody, settlement, compliance architecture, and the regulatory standing. All of that determines where they can operate and which products they can offer. Others are anchoring around a defined user segment. They prioritise depth of service over breadth, whereas a third group is moving beyond trading entirely. They compete for payment flows, settlement infrastructure, and financial services aimed at users who may never trade at all. These three strategic orientations form the basis for the archetypes that follow.

The Competitive Outlook: Where the Market Is Heading

The Three Types of Exchanges’ Strategy

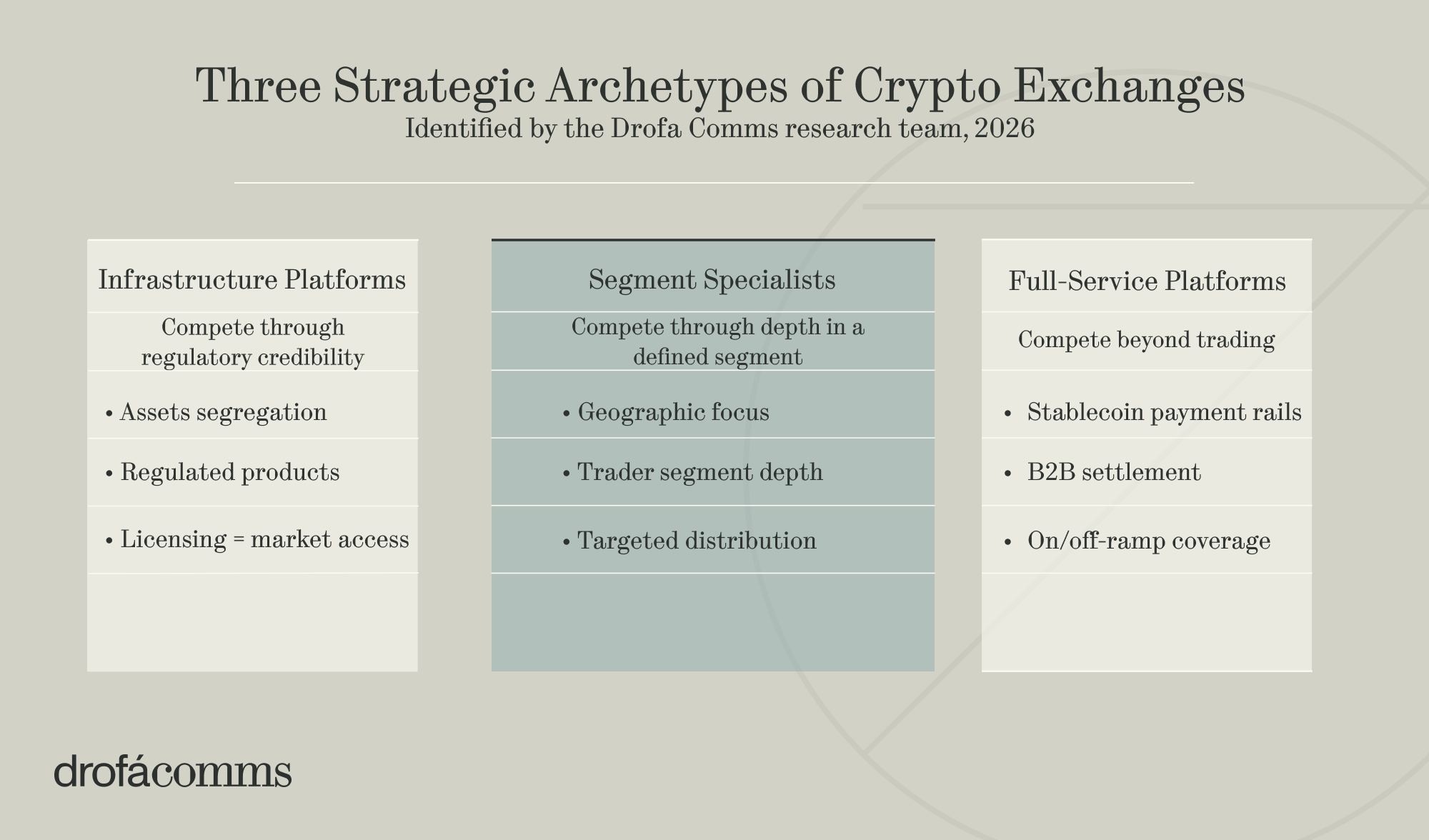

Based on the research conducted for this report, the Drofa Comms team identifies three distinct strategic archetypes. These are not rigid categories. Some exchanges exhibit traits associated with more than one model. Even so, the the area where each platform invests most heavily, determines where it aligns most closely.

One pattern runs across all three archetypes: AI. Every exchange examined in this research deploys AI in the same core areas. They are fraud detection, compliance screening, support triage, and trade execution. Because AI functions as operational infrastructure for the sector as a whole, it does not constitute a separate archetype. It is a baseline capability. The evidentiary basis for the typology should also be noted. The framework draws on publicly available information from Coinbase, Kraken, Binance, OKX, and Bitget. It is also supplemented by direct questionnaire responses from KuCoin and Bitunix. It is presented as an interpretive structure for understanding the strategic directions visible in the market.

- The Institutional Platforms

The first archetype consists of exchanges that have built their infrastructure around the requirements of supporting institutional capital inflows at scale. Their core investment goes toward custody, asset segregation, settlement, and access to regulated products. These are the functions institutional clients examine before allocating capital to a platform. Within this model, regulatory licensing is a condition of commercial expansion. It determines which markets an exchange can enter, which products it can offer, and which institutional partnerships it can pursue. Among the exchanges examined in this research, Kraken, Binance, Bitget, and OKX most explicitly reflect this cohort.

This is a long-cycle model. The infrastructure is costly to build, regulatory credibility takes years to establish, and commercial returns emerge gradually. Once these exchanges reach the threshold, it becomes difficult to displace them. Institutional switching costs are high, while the barriers facing new competitors seeking to enter the same space are higher still.

- The Segment Specialists

The second archetype consists of exchanges that have chosen depth over breadth, anchoring in a specific geography or trader segment instead of competing across the entire market. Product design, distribution, and partnerships are all built around a defined user profile rather than around maximum coverage.

This model can produce stronger retention and lower acquisition costs inside the target segment. It also reduces direct competition with the largest global platforms. Its weakness lies in concentration. If the target segment changes materially these platforms have limited ability to absorb the impact. This is because both their user base and their revenues are tied closely to a single audience. Bitunix, with its focus on active professional traders in Southeast Asia and Latin America, represents this archetype most directly in the research.

- The Full-Service Platforms

The third archetype consists of exchanges that are extending their offering beyond trading. Stablecoin payment rails, B2B settlement infrastructure, broad on- and off-ramp coverage, and wider financial services are built into the platform alongside execution. In this model, trading is becoming one function within a broader financial system rather than the primary product around which everything else sits.

This approach opens a different revenue base. Exchanges in this category are competing for payment flows, treasury activity, and cross-border settlement. Therefore, they attract users and counterparties who may never open a trading position. The ambition is considerable, and so is the risk. Building payments infrastructure at this scale requires established banking partnerships, regulatory approvals across multiple jurisdictions, and internal systems. Many exchanges still do not possess them. Coinbase, with its explicit aim of becoming an “Everything Exchange,” is the clearest example of this archetype in the research. KuCoin’s strategic positioning also aligns with this model.

What the Market Will Look Like by 2030

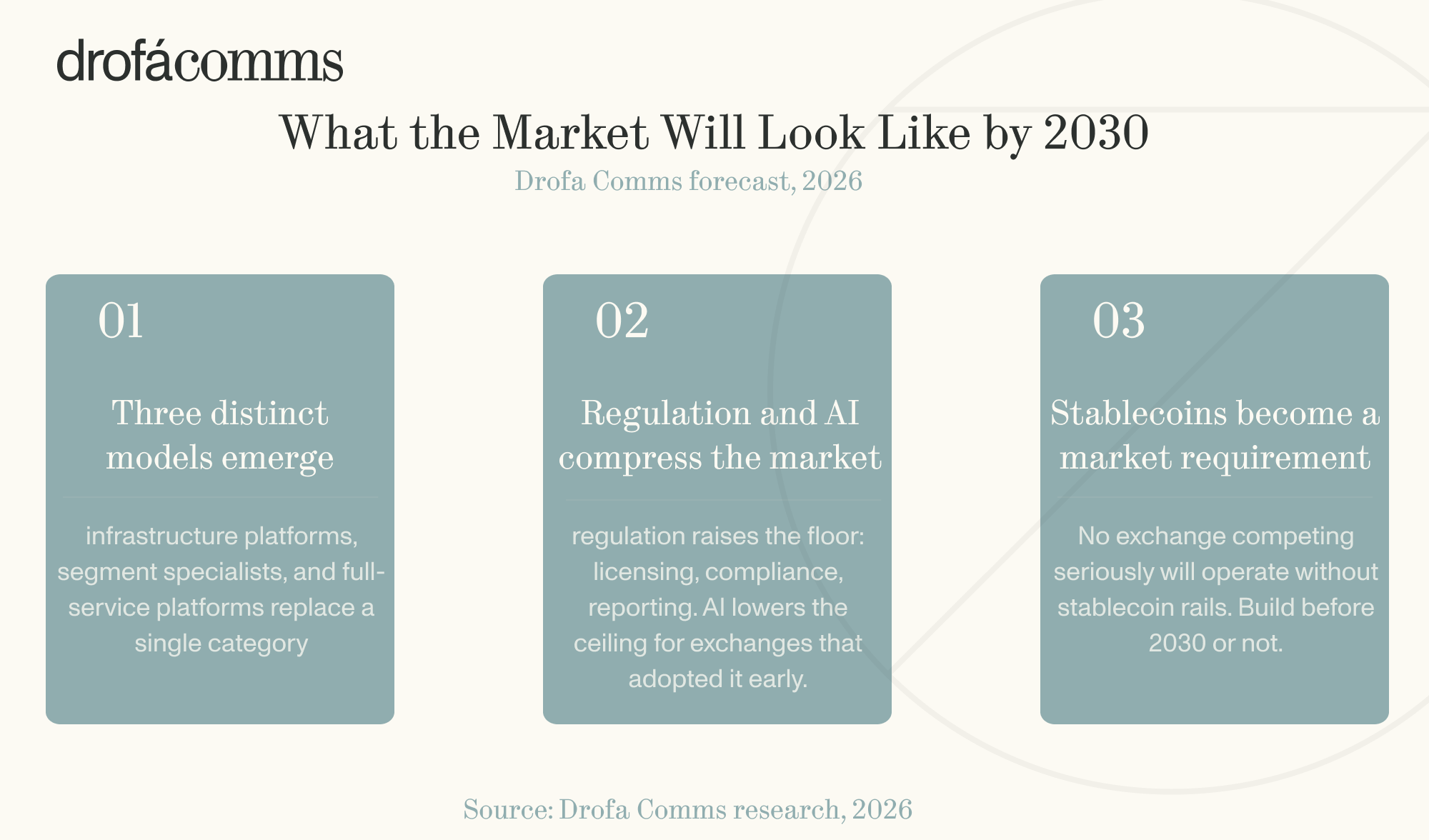

The strategic directions visible across crypto exchanges in 2026 now support several conclusions about where the market is likely to be by 2030.

- The exchange category will have reorganised around three distinct models

By 2030, the term “crypto exchange” will describe three different types of business. The first will be institutional infrastructure. That means platforms closer to traditional financial venues than to the exchanges of 2017 or 2021. They build around custody, settlement, and regulated product access. The second are segment-focused platforms. This means they have gone deep in particular geographies or trader profiles rather than competing throughout the market. The third will be the financial super-app: payment-enabled, stablecoin-native, with trading positioned as one function among several.

The middle ground, namely platforms that have made no clear commitment among these directions, is likely to narrow. Some will be acquired. Others will lose users and volume gradually as capital consolidates around stronger propositions. The underlying dynamic is that undifferentiated exchanges face simultaneous pressure from several directions. Compliance costs rise faster than they can be spread across revenue, institutional clients remain beyond reach because no one meets required standards, and serious retail users migrate toward platforms that perform better under stress.

- Regulation and AI will compress the market from opposite ends

Within the next five years, the regulatory frameworks now taking shape, including MiCA, the FCA regime, APAC licensing structures, and federal legislation in the United States, will have had time to exert full effect. The result is likely to be a tiered market: exchanges with full regulatory standing in major jurisdictions on one side, and exchanges operating where requirements remain lighter on the other. The first group will attract institutional capital, banking partnerships, and access to regulated products. The second will compete more heavily on price and accessibility.

At the same time, AI will have widened the operating cost gap between platforms. Exchanges that embedded it into core workflows by 2026 will carry materially lower cost structures than those that treated it as a superficial add-on. In financial markets, margins narrow as competition intensifies. When more platforms compete for the same users and volume, fees compress, and those with higher cost basis face pressure first.

These forces reinforce one another. Regulation raises the floor cost of operating in major markets. It does so through licensing fees, compliance systems, reporting obligations, and the personnel. AI lowers the ceiling cost for exchanges that have adopted it deeply. The net result is that exchanges caught between these two pressures. They carry full regulatory costs without corresponding efficiency gains from AI. So they are more likely to face the sharpest margin compression. This is where the mid-tier appears most exposed.

- Stablecoin integration will have become a market entry requirement.

This applies across all three archetypes, even if the degree differs. By 2030, no exchange is likely to compete seriously without some form of stablecoin integration. Payment rails, on- and off-ramp infrastructure, and B2B settlement capabilities established before 2030 will be difficult to replicate later, because the partnerships, regulatory approvals, and distribution channels that support them take years to build.

For Full-Service Platforms, stablecoin infrastructure is a core product. Institutional Platforms, in turn, should treat it as a settlement layer that institutional clients will expect as standard. For Segment Specialists, it is the on-ramp that determines whether users in underbanked markets can access the platform at all. In each case, the exchange that has already built this capability holds a strategic advantage over the one still trying to assemble it.

Recommendations for Crypto Exchanges in 2026

The first step is to choose a strategic direction from the three the market is now forming around. These are building institutional infrastructure, going deep in a defined segment, or extending beyond trading into payments. Exchanges that make a clear choice about the model they are building toward are in a stronger position to allocate resources, build trust, and attract the partners they need.

Compliance should stand for a market-entry instrument rather than as a legal overhead alone. Exchanges that secure the necessary licences before expanding into new markets will be able to enter and scale faster than those that address regulatory requirements only after the fact. The same logic applies to institutional infrastructure. Custody standards, settlement systems, and reporting capabilities need to be in place before institutional clients arrive, not after.

On the retail side, the moments that determine whether users remain with a platform are rarely about feature breadth. Slow withdrawals, unresolved support tickets, and outages during volatile periods are what serious users remember. Closing those gaps should take precedence over adding functionality. On the technology side, AI delivers measurable value only when it is in core workflows and when someone oversees its deployment. Used as a surface-level feature, it creates integration cost without producing the efficiency gains that justify adoption.

Conclusion

After examining what crypto exchanges are doing in 2026 to remain competitive through 2030, and the forces shaping the market around them, one conclusion stands out: the cost of remaining generic is rising.

Institutions now require operational standards that broad, undifferentiated platforms cannot meet. Serious retail users are making platform choices based on reliability under stress rather than on feature count. Regulation is creating a tiered market in which access to capital, products, and partnerships increasingly depends on regulatory standing. AI, meanwhile, is widening the efficiency advantage of exchanges that have embedded it deeply. This makes the competition harder for those that have not done so.

Taken together, these forces are reorganising the market around a smaller number of more defined platforms. The exchanges gaining ground share three characteristics. They have deeper infrastructure, clearer strategic positioning, and stronger control over the functions that determine their standing. By 2030, the leading exchanges are likely to be those that made deliberate choices early. The decisions are about whom they serve, what they build, and which markets they are preparing to enter.

“If an exchange doesn’t have its own identity in 2026, it risks dissolving into the crowd. Today the market is rewarding precision in everything: in the clients you target, the products you build, the licences you pursue. Above all is the story you tell. By 2030, that precision will have made all the difference.” — Valentina Drofa, CEO and Founder of Drofa Comms.

Acknowledgments

The Drofa Comms research team thanks KuCoin and Bitunix for participating directly in this research. Their responses added a perspective that public data alone cannot provide — a view from inside the strategic decisions shaping the market in real time.